You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

12:08 - Redux

- Thread starter Devvy

- Start date

Devvy

Donor

Cheers, quickly sorted I think. Lack of sleep!Pullman 3 description seems to have been cut short.

")

Cheers, quickly sorted I think. Lack of sleep!

Indeed...I assume you've seen the footage of the existing IC125 in Blue Pullman colours?

Devvy

Donor

Indeed...I assume you've seen the footage of the existing IC125 in Blue Pullman colours?

Yeah it popped up online!

Controversial opinion though; I'm not a massive fan of the livery.

Some thoughts to spitball;I wonder what the effects of all this were on Britain as a whole...

- Domestic aviation within GB largely killed off except for some Anglo-Scottish routes.

- Nottingham becomes popular amongst richer London commuters due to cheaper homes and fast links to central London.

- More Govt departments and public sectors relocate to Manchester due to fast links.

- Leeds continues to specialise and excel in banking outside the big big financial institutions in London.

- Post 2007 has direct services to Paris from regional locations. Maybe a bit more "Europeanisation" of areas such as Nottingham, especially in conjunction with the second point?

I didn't think much of the livery originally either but it seems to look better on the HST than the original design.Yeah it popped up online!

Controversial opinion though; I'm not a massive fan of the livery.

Some thoughts to spitball;

- Domestic aviation within GB largely killed off except for some Anglo-Scottish routes.

- Nottingham becomes popular amongst richer London commuters due to cheaper homes and fast links to central London.

- More Govt departments and public sectors relocate to Manchester due to fast links.

- Leeds continues to specialise and excel in banking outside the big big financial institutions in London.

- Post 2007 has direct services to Paris from regional locations. Maybe a bit more "Europeanisation" of areas such as Nottingham, especially in conjunction with the second point?

Devvy

Donor

I do like the Pullman livery.

Interesting that the Haddington Branch survives.

My intention wasn't that it's survived, but that the alignment is still there (roughly as per OTL) allowing a reintroduction of trackwork and rail services if desired (if there is capacity to run in to Waverley).

Would you say that Britain is more economically prosperous to a noticeable degree compared to OTL. And if not the whole nation, are there any specific areas which have benefitted?Yeah it popped up online!

Controversial opinion though; I'm not a massive fan of the livery.

Some thoughts to spitball;

- Domestic aviation within GB largely killed off except for some Anglo-Scottish routes.

- Nottingham becomes popular amongst richer London commuters due to cheaper homes and fast links to central London.

- More Govt departments and public sectors relocate to Manchester due to fast links.

- Leeds continues to specialise and excel in banking outside the big big financial institutions in London.

- Post 2007 has direct services to Paris from regional locations. Maybe a bit more "Europeanisation" of areas such as Nottingham, especially in conjunction with the second point?

Good old Pullman!

Wonder what colours Pullman trains have here?

Anyway I wonder if the whole Highland line between Perth and Inverness has been doubled to allow pathing space for frient trains with I can imagine links on with the Waverley and S&C lines creating a mostly freight rail link.

Anyway with the recent news on the Isle of Wight, what changes are there compared to OTL such as using D78 stock or track to Ventnor?

Wonder what colours Pullman trains have here?

Anyway I wonder if the whole Highland line between Perth and Inverness has been doubled to allow pathing space for frient trains with I can imagine links on with the Waverley and S&C lines creating a mostly freight rail link.

Anyway with the recent news on the Isle of Wight, what changes are there compared to OTL such as using D78 stock or track to Ventnor?

Very cool Pullman poster there.

Poor Birmingham losing out to Manchester.

Same with Cardiff not being connected to Pullman. Bet that get certain political parties a few votes from annoyance at 'being ignored by Westminster...'

That is such a fast timetable compared to anything OTL. Nicely worked out.

Double decker trains would be kinda cool to see in the UK. When you have your own rails to play with I guess its easier.

The tunnel to Edinburgh sounds like the sort of expansion that just makes sense- unlike the 'cool engineering, but actually required?' Irish tunnel.

I am actually surprised Leicester missed out if Pullman goes straight through, esp that it has taken so long ITTL to get an alt sorted.

I am fairly sure you said the intercity roll on-drive off 'car-ferries' service did not survive - but does the existence of the Chunnell see any demand for such a service from say Cardiff, Edinburgh etc - drive on and drive off in France?

Poor Birmingham losing out to Manchester.

Same with Cardiff not being connected to Pullman. Bet that get certain political parties a few votes from annoyance at 'being ignored by Westminster...'

That is such a fast timetable compared to anything OTL. Nicely worked out.

Double decker trains would be kinda cool to see in the UK. When you have your own rails to play with I guess its easier.

The tunnel to Edinburgh sounds like the sort of expansion that just makes sense- unlike the 'cool engineering, but actually required?' Irish tunnel.

I am actually surprised Leicester missed out if Pullman goes straight through, esp that it has taken so long ITTL to get an alt sorted.

I am fairly sure you said the intercity roll on-drive off 'car-ferries' service did not survive - but does the existence of the Chunnell see any demand for such a service from say Cardiff, Edinburgh etc - drive on and drive off in France?

Devvy

Donor

Would you say that Britain is more economically prosperous to a noticeable degree compared to OTL. And if not the whole nation, are there any specific areas which have benefitted?

Economics isn't my strong point, but on the assumption that GB is not more prosperous, the existing OTL-like prosperity is a little more spread across the UK - particularly within England where Pullman to the North-West and to Yorkshire has been running for several decades now. For those in Nottingham who commute to London a few times a week by Pullman are bringing their London wages to the East Midlands, Manchester will see more government and public bodies locating there, Leeds will see more regional banks clustering there. Even though it's not Pullman, the existence of better cross-Pennine train services with "Transpennine High Speed" means that Liverpool, Manchester, Leeds and to a lesser extent Sheffield can act as a single cluster which has economic advantages.

Good old Pullman!

Wonder what colours Pullman trains have here?

Anyway I wonder if the whole Highland line between Perth and Inverness has been doubled to allow pathing space for frient trains with I can imagine links on with the Waverley and S&C lines creating a mostly freight rail link.

Anyway with the recent news on the Isle of Wight, what changes are there compared to OTL such as using D78 stock or track to Ventnor?

My vision for Pullman in 2020 would be something like the GNER dark blue with a red stripe livery - to me it seems rather stylish, corporate and "prestigey". Fits right in with the product placement for Pullman.

Highland Line; I'd imagine Scotrail, probably around the same time as OTL, wants to double the route, at least to Aviemore where the branches to Inverness and Elgin separate.

And for the IoW, I think we mentioned a while ago it's increasingly run as a local metro service; I think we said that older LU stock is in use as well, although probably still maintained a little better than OTL. Ryde to Newport and Ryde to Ventnor still operate, with significant stretches of double track to allow a decent operation in summer time. The hoped for cross-Solent link will connect the 2 IoW branches to the mainland (no road tunnel to avoid road congestion).

Very cool Pullman poster there.

Poor Birmingham losing out to Manchester.

Same with Cardiff not being connected to Pullman. Bet that get certain political parties a few votes from annoyance at 'being ignored by Westminster...'

That is such a fast timetable compared to anything OTL. Nicely worked out.

Double decker trains would be kinda cool to see in the UK. When you have your own rails to play with I guess its easier.

The tunnel to Edinburgh sounds like the sort of expansion that just makes sense- unlike the 'cool engineering, but actually required?' Irish tunnel.

I am actually surprised Leicester missed out if Pullman goes straight through, esp that it has taken so long ITTL to get an alt sorted.

I am fairly sure you said the intercity roll on-drive off 'car-ferries' service did not survive - but does the existence of the Chunnell see any demand for such a service from say Cardiff, Edinburgh etc - drive on and drive off in France?

Birmingham in in the niche of positions where it's not that far to London, Manchester, Nottingham etc, so the high speed time savings are not so great. Brum does get a very intensive train service though - I think we said something like a train every 10 minutes to London. South Wales just doesn't have the economic pull; they have Pullman-1 trains operating the route, likely at around 100-110mph though, and the better acceleration means that it's probably similar timings to OTL but with higher capacity trains.

Leicester Central being skipped originally; the station closed in the 1960s anyway, when the GCML was used more as a freight corridor. Just not rebuilt in order to better serve the north to London without too many intermediate station stops, and also as Leicester isn't a) a major city and b) particularly far away from London - the time savings of Pullman over "normal" services wouldn't have been that great.

Not sure on your point exactly for the car ferries?

(sorry, written in a bit of a rush whilst working!

)

2020-Finale-Finale!

Devvy

Donor

2020 - Final Thoughts

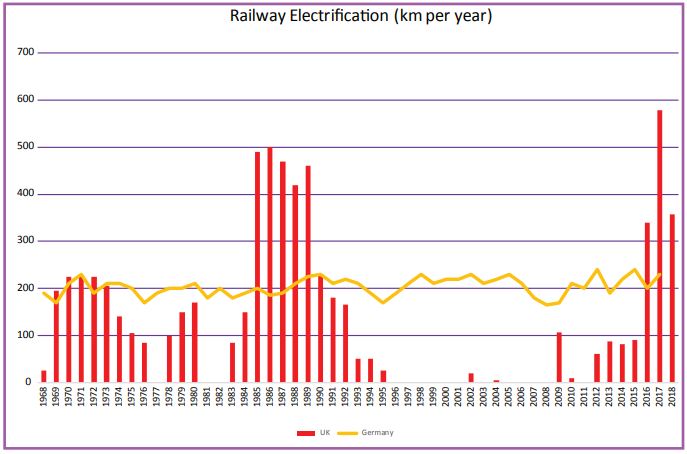

Electrification

Obviously there's a lot, lot more of it in this TL. And it's the older standard of 1.5kV DC largely (bar Pullman). 1.5kV DC was the original proposal for widespread electrification, but it does have several disadvantages over the more modern 25kV AC; a thicker overhead wire is needed for the higher current, and you need feeder stations more frequently. On the flip side, it's a very simple system and works well - it has higher power (and overhead instead of third rail) over the OTL south eastern third rail system, and that has gently expanded over the decades. The 1.5kV DC system with makes it well suited to urban/city network electrification, which we've done often here - most city areas are electrified, and some of the main lines. Roughly speaking, there's been one city network and one long main line electrified every 10 or so years, with an interest in creating wider networks, eliminating short stubs of non electrification (so that fully electric trains instead of hybrids can be used, and the hybrids can then be sent elsewhere).

I see electrification being much cheaper than OTL; OTL is about £1m to £2m per single track kilometre (stk), depending on complexity. Most projects in Europe run far below that, as they retain institutional knowledge in the supporting works (erecting gantry in stations, etc etc etc); overhead electrification only projects in Germany and Switzerland are recorded at an average of approx £400k per stk - less than half the cost in OTL of GB. Part of this is due to the wider loading gauge, so granted it's a little easier, but also the financials are easier to sort rather than the complex contractual refunds Network Rail pays to close railways (and especially if slight delays!), and contracts are awarded far in advance of work starting, so works can be queued up and teams move from one project to the next, retaining experience and skills. In light of this, I think in this TL, the rolling works of BR to electrify will make the cost of electrification far cheaper (maybe by todays standards around £0.75m-£1m per stk), which allows a smaller pot of recurring taxmoney to pay for continuous electrification works.

Trains

Compared to OTL, there's more electric traction as discussed. This means more electric multiple units, but also the wider spread means that hybrid multiple units are more popular as they run under electric wires for a greater proportion of their journey, so investing in dual/hybrid traciton is worth while. I think you'll see "modern" electric multiple units, whilst hybrid trains will be older units, like the Sprinters we still have around, which are moved around and continously used - no point in buying new ones as electric wires spread. There's much less variety in train types - urban, regional, Intercity - rather than the cocophony of train types we have in OTL. The fewer types means longer production runs, meaning greater supply chain reliability, more compatible systems (from memory I think in OTL there are 5 or 6 different, and non-compatible, multiple working signalling/coupling types), and easier serviceability.

Route network

Wider than OTL; but bear in mind a large number of cuts in OTL came *before* Beeching, which have roughly speaking stayed in place in ITTL. They closed for good reason; small, unused, rural, money-sinks. Other routes stayed open initially, but there was still a "slow burn" of routes, so more stayed open, but some continued to close - although some which closed were either retained for re-opening, or passed to local Govt control for local transit. Obviously the eye-catchers are the Great Central staying open and becoming a Pullman route, the Waverley Route in Scotland (and Aberdeen network). But lots of smaller routes too. There have also been losers; the East Coast never got it 1980s upgrade. Local transit; the urban networks taking away BR's de facto peak time railway in regional cities is the big winner, with many local transport authorities taking over networks. Manchester, Liverpool, Newcastle, etc etc - they all have decent networks now, and BR gets to walk away from complex peak time networks which are far less used during off-peak. BR more concentrating on regional and long-distance service.

Costs

I guess this is a big one. I'd like to think ticket price would be cheaper; I definitely feel a decent portion of OTL ticket cost goes on "artificial arrangements" - contractual commitments, services (ie. HR for each company), train leasing at inflated ROSCO prices, etc etc. And the wider electrification will reduce fuel costs which are a significant part too. However, BR is a public body, and they never do well at union disputes or business efficiency it has to be said. So maybe a bit lower, but not that much. I think passenger numbers will have risen massively in the 2010s, as per OTL, and significantly surpassed OTL; instead of 1.75bn passengers in 2019, maybe over 2bn. More routes, larger Pullman trains, slightly cheaper costs, and much better service in the populated Transpennine region. I'm a firm believer that the post-privatisation OTL rise in passenger numbers was driven by the economy (and road congestion/congestion charging) rather than anything specific the train operators did, so that would be reflected on BR tool.

Railfreight

I think Speedlink (ie. freight wagons) was a dying network, but may have continued if it could have been converted to container boxes instead for rail operations, and possibly marshalling yards (electric wire-free) with cranes moving boxes between trains quickly and efficiently. Who knows. I think container trains from docks to inland yards, and via the Channel Tunnel would have been greater, especially with Pullman taking many of the high speed trains out of the way, and a greater route network to avoid busy areas - and wider electrification for cheaper operation.

Privatisation

I think something was almost guaranteed in the political climate of the 1990s. The small route operators are perhaps the best way of doing this; they create networks which are financially viable, long lease times encourage the private operator to invest in the network with a real chance of getting a reward for it, and also galvanise opposition to wider privatisation of BR!

And there's a brain dump of remaining thoughts I've churned out for 15 mins, just to bring this to a final close after over 2 years! Maybe an appendix or two if I have time and the motivation one day!

Electrification

Obviously there's a lot, lot more of it in this TL. And it's the older standard of 1.5kV DC largely (bar Pullman). 1.5kV DC was the original proposal for widespread electrification, but it does have several disadvantages over the more modern 25kV AC; a thicker overhead wire is needed for the higher current, and you need feeder stations more frequently. On the flip side, it's a very simple system and works well - it has higher power (and overhead instead of third rail) over the OTL south eastern third rail system, and that has gently expanded over the decades. The 1.5kV DC system with makes it well suited to urban/city network electrification, which we've done often here - most city areas are electrified, and some of the main lines. Roughly speaking, there's been one city network and one long main line electrified every 10 or so years, with an interest in creating wider networks, eliminating short stubs of non electrification (so that fully electric trains instead of hybrids can be used, and the hybrids can then be sent elsewhere).

I see electrification being much cheaper than OTL; OTL is about £1m to £2m per single track kilometre (stk), depending on complexity. Most projects in Europe run far below that, as they retain institutional knowledge in the supporting works (erecting gantry in stations, etc etc etc); overhead electrification only projects in Germany and Switzerland are recorded at an average of approx £400k per stk - less than half the cost in OTL of GB. Part of this is due to the wider loading gauge, so granted it's a little easier, but also the financials are easier to sort rather than the complex contractual refunds Network Rail pays to close railways (and especially if slight delays!), and contracts are awarded far in advance of work starting, so works can be queued up and teams move from one project to the next, retaining experience and skills. In light of this, I think in this TL, the rolling works of BR to electrify will make the cost of electrification far cheaper (maybe by todays standards around £0.75m-£1m per stk), which allows a smaller pot of recurring taxmoney to pay for continuous electrification works.

Trains

Compared to OTL, there's more electric traction as discussed. This means more electric multiple units, but also the wider spread means that hybrid multiple units are more popular as they run under electric wires for a greater proportion of their journey, so investing in dual/hybrid traciton is worth while. I think you'll see "modern" electric multiple units, whilst hybrid trains will be older units, like the Sprinters we still have around, which are moved around and continously used - no point in buying new ones as electric wires spread. There's much less variety in train types - urban, regional, Intercity - rather than the cocophony of train types we have in OTL. The fewer types means longer production runs, meaning greater supply chain reliability, more compatible systems (from memory I think in OTL there are 5 or 6 different, and non-compatible, multiple working signalling/coupling types), and easier serviceability.

Route network

Wider than OTL; but bear in mind a large number of cuts in OTL came *before* Beeching, which have roughly speaking stayed in place in ITTL. They closed for good reason; small, unused, rural, money-sinks. Other routes stayed open initially, but there was still a "slow burn" of routes, so more stayed open, but some continued to close - although some which closed were either retained for re-opening, or passed to local Govt control for local transit. Obviously the eye-catchers are the Great Central staying open and becoming a Pullman route, the Waverley Route in Scotland (and Aberdeen network). But lots of smaller routes too. There have also been losers; the East Coast never got it 1980s upgrade. Local transit; the urban networks taking away BR's de facto peak time railway in regional cities is the big winner, with many local transport authorities taking over networks. Manchester, Liverpool, Newcastle, etc etc - they all have decent networks now, and BR gets to walk away from complex peak time networks which are far less used during off-peak. BR more concentrating on regional and long-distance service.

Costs

I guess this is a big one. I'd like to think ticket price would be cheaper; I definitely feel a decent portion of OTL ticket cost goes on "artificial arrangements" - contractual commitments, services (ie. HR for each company), train leasing at inflated ROSCO prices, etc etc. And the wider electrification will reduce fuel costs which are a significant part too. However, BR is a public body, and they never do well at union disputes or business efficiency it has to be said. So maybe a bit lower, but not that much. I think passenger numbers will have risen massively in the 2010s, as per OTL, and significantly surpassed OTL; instead of 1.75bn passengers in 2019, maybe over 2bn. More routes, larger Pullman trains, slightly cheaper costs, and much better service in the populated Transpennine region. I'm a firm believer that the post-privatisation OTL rise in passenger numbers was driven by the economy (and road congestion/congestion charging) rather than anything specific the train operators did, so that would be reflected on BR tool.

Railfreight

I think Speedlink (ie. freight wagons) was a dying network, but may have continued if it could have been converted to container boxes instead for rail operations, and possibly marshalling yards (electric wire-free) with cranes moving boxes between trains quickly and efficiently. Who knows. I think container trains from docks to inland yards, and via the Channel Tunnel would have been greater, especially with Pullman taking many of the high speed trains out of the way, and a greater route network to avoid busy areas - and wider electrification for cheaper operation.

Privatisation

I think something was almost guaranteed in the political climate of the 1990s. The small route operators are perhaps the best way of doing this; they create networks which are financially viable, long lease times encourage the private operator to invest in the network with a real chance of getting a reward for it, and also galvanise opposition to wider privatisation of BR!

And there's a brain dump of remaining thoughts I've churned out for 15 mins, just to bring this to a final close after over 2 years! Maybe an appendix or two if I have time and the motivation one day!

Last edited:

I can see this BR being very interesting in wind and solar tech as it becomes viable in the early 21stC as a way of lowering its electricity bill.

The splintering of train sets and such must partly be a result of privatisation and no 'one hand on the tiller' guiding the train companies what to buy unlike ITTL. Fewer train types probably helps build up brand identification ITTL.

Agree on ticket prices. Admin costs a possibly lower on a less fragmented network.

Rail freight gets a better deal ITTL I think. A quick move to containers will help. More routes also def keeps more options open for keeping freight services. Perhaps people like Amazon, Argos etc take premises near rail lines and have fright trains deliver directly into their depots?

If BR keep the Conservatives happy with City networks, light rail projects, costs reductions (like the rolling electrification project), and better labour relations then I could see there being less demand for Privatising the whole company.

I do wonder how much 'ripple effect' in national politics, personal romances, goods delivery, car ownership, tourism etc this Timeline produces- but that we will never know.

Overall this timeline feels very plausible to me, you have not gone for a Utopian version of BR, but something that feels quite realistic.

Thank you.

The splintering of train sets and such must partly be a result of privatisation and no 'one hand on the tiller' guiding the train companies what to buy unlike ITTL. Fewer train types probably helps build up brand identification ITTL.

Agree on ticket prices. Admin costs a possibly lower on a less fragmented network.

Rail freight gets a better deal ITTL I think. A quick move to containers will help. More routes also def keeps more options open for keeping freight services. Perhaps people like Amazon, Argos etc take premises near rail lines and have fright trains deliver directly into their depots?

If BR keep the Conservatives happy with City networks, light rail projects, costs reductions (like the rolling electrification project), and better labour relations then I could see there being less demand for Privatising the whole company.

I do wonder how much 'ripple effect' in national politics, personal romances, goods delivery, car ownership, tourism etc this Timeline produces- but that we will never know.

Overall this timeline feels very plausible to me, you have not gone for a Utopian version of BR, but something that feels quite realistic.

Thank you.

Devvy

Donor

I can see this BR being very interesting in wind and solar tech as it becomes viable in the early 21stC as a way of lowering its electricity bill.

The splintering of train sets and such must partly be a result of privatisation and no 'one hand on the tiller' guiding the train companies what to buy unlike ITTL. Fewer train types probably helps build up brand identification ITTL.

Agree on ticket prices. Admin costs a possibly lower on a less fragmented network.

Rail freight gets a better deal ITTL I think. A quick move to containers will help. More routes also def keeps more options open for keeping freight services. Perhaps people like Amazon, Argos etc take premises near rail lines and have fright trains deliver directly into their depots?

If BR keep the Conservatives happy with City networks, light rail projects, costs reductions (like the rolling electrification project), and better labour relations then I could see there being less demand for Privatising the whole company.

I do wonder how much 'ripple effect' in national politics, personal romances, goods delivery, car ownership, tourism etc this Timeline produces- but that we will never know.

Overall this timeline feels very plausible to me, you have not gone for a Utopian version of BR, but something that feels quite realistic.

Thank you.

Glad you enjoyed it; definitely not utopian, hopefully realistic for what may have been possible. Agreed for almost all your comments!

Devvy

Donor

Maybe I've misunderstood you, but in this TL, the GCML forms the backbone of the Pullman route from Aylesbury north?So are we at an end? Part of me wishes that the GCR survived at least as seeing it take HS2 ITTL would be good for all

Sorry mate, meant Pullman here.Maybe I've misunderstood you, but in this TL, the GCML forms the backbone of the Pullman route from Aylesbury north?

2020-Finale-8-Bonus

Devvy

Donor

2020 Roundup - Regional Stations

Harrogate

Crimple Viaduct, and a steam train approaching Harrogate.

Harrogate lies at the middle of a set of junctions north of Leeds, and once had a bypass route to the east avoiding the city centre as well as a wide array of branch lines in to various dales. By the 1960s the writing was on the wall for the smaller branches. The Harrogate bypass line closed in the 1950s, with all traffic operating via Harrogate station itself using a very tight curve and junction adjacent to Pateley Bridge, having already closed to passengers in the early 1950s, lost it's good service and entire branch line in the 1960s, a pattern copied closely on the branch to small Boroughbridge from nearby Knaresborough.

All this left Harrogate in it's current position, flanked to north and south by two sets of lines; to Northallerton and York to the north, and to Leeds (via Horsforth or via Wetherby) to the south. Evolving patterns of service, reflecting particularly the growing commuter trip from wider Harrogate area to Leeds for work & shopping, and to a lesser extent, York, occurred over the decades. A Leeds (via Horsforth and Harrogate) local service was later bouyed by the construction of new housing along the line outside York, whilst the local Leeds service (via Wetherby) became popular with Leeds commuters there and terminated at Harrogate. Finally, a Leeds to Newcastle or Middlesbrough semi-express service ran via Horsforth, Harrogate and Ripon, connecting the stations to the North-East, and lately, destinations in South Yorkshire.

The amount of services passing through Harrogate - all stopping at the major station, placed a strain on a station with only 2 platforms, and trying to accommodate terminating local services from Wetherby. The aging station was largely demolished in the 1980s, and the station significantly redesigned. Gone were the 2 platforms, and 4 tracks in the station area (including 2 middle bypass tracks). The western bay platforms and redundant tracks disappeared, and land turned over to the council to create a larger bus station with more covered waiting areas. The platforms and trackwork were redesigned to give 3 platforms (the western platform being kept), with the eastern (Leeds-bound) track removed, moved to the east, and then an island platform inserted to give a central "terminating" platform. The station building was also demolished and rebuilt, incorporating new direct bridge links to the enlarged bus station, adjacent multi-storey car park, and a cross-road bridge to the town centre (and later also a shopping centre), giving a very small "Pedway" network.

Lincoln

An aerial view of Lincoln from decades gone by, showing both Central and St Marks stations.

Lincoln, for many decades, had the dubious honour of being endowed with two separate stations, catering to differing routes. Lincoln Central existed on the Northwest - Southeast axis (roughly Yorkshire to East Anglia), whilst Lincoln St Marks sat on a Southwest - Northeast axis (roughly East Midlands to the Lincolnshire coast). Although the lines intersected on a flat diamond crossing, causing a bottleneck, the stations remained separate until the 21st Century. Other branches from the two stations had, by then, closed; the branch network to Louth, Boston and Skegness was well gone, whilst the arrangement of Lincoln bypass lines around the town centre were on their last legs. The branch line to the west to Mansfield only existed in order to allow coal trains access to the significant power station complex at High Marnham. Upon closure of High Marnham during the 1990s switch from coal to gas, the site was procured by British Rail and used during initial experiments in to wind turbines and how much electricity they could contribute to British Rail (in order to reduce their energy costs). By now, the branch via Market Rasen to Grimsby was hardly used, with a very derelict station at Market Rasen; most rural passengers used Louth instead, which still retained direct London services from Grimsby, and there were few longer distance passengers from the Grimsby area to the East Midlands.

Whilst officially open, in the 1990s the Market Rasen branch was mothballed, it's role in the network dead with freight now running via Louth or Gainsborough (where a new short chord allowed multi-directional access), and very few passengers using Market Rasen station itself. The line to Mansfield also became redundant after the closure of High Marnham in the 1990s too, with the line to be closed - until the Mansfield Heritage Railway stepped in. The railway, using a site on the eastern outskirts of Mansfield on the former Mansfield Railway route, raised capital and acquired the line to Lincoln, as well as the rights to use the Lincoln St Marks site (as trains services east of St Marks towards Market Rasen were no longer operating). A new "Lincoln Rail 2010" plan was launched in 2000; works would be conducted to remove level crossings; both to the east (Great Northern Terrace - to receive a road overbridge), and in the town centre. The High Street crossing would be pedestrianised (in line with a local council objective) and replaced by a large overbridge, which would continue over Wigford Way / St Marys Street, although plans to close the Brayford Wharf crossing were voted down by the local council and the level crossing remains, albeit with a footbridge. The British Railways route from Newark now approached Lincoln in a slightly twisted fashion with a triangular junction, whilst the newly extended heritage line (now the Mansfield & Lincoln Railway) now using a bridge over the BR tracks, nicknamed the "ski jump" due to the gradients operated to Lincoln St Marks station. The M&L Railway has one of the longest stretches of double track of all British heritage routes, and operates intensively on summer weekends.

-------------

Well thank you for the honour in the Turtledove thread. In return, here's a bonus little chapter of material that I hadn't got round to fleshing out !

Harrogate is a semi-important junction stations, with a retained line via Wetherby and also via Ripon to the north. Lincoln is less busy; the line via Market Rasen has virtually closed - I'd bet there'd be "Mansfield & Lincoln Railway" people eying up an extension there, but at the moment it's just mothballed.

Harrogate

Crimple Viaduct, and a steam train approaching Harrogate.

Harrogate lies at the middle of a set of junctions north of Leeds, and once had a bypass route to the east avoiding the city centre as well as a wide array of branch lines in to various dales. By the 1960s the writing was on the wall for the smaller branches. The Harrogate bypass line closed in the 1950s, with all traffic operating via Harrogate station itself using a very tight curve and junction adjacent to Pateley Bridge, having already closed to passengers in the early 1950s, lost it's good service and entire branch line in the 1960s, a pattern copied closely on the branch to small Boroughbridge from nearby Knaresborough.

All this left Harrogate in it's current position, flanked to north and south by two sets of lines; to Northallerton and York to the north, and to Leeds (via Horsforth or via Wetherby) to the south. Evolving patterns of service, reflecting particularly the growing commuter trip from wider Harrogate area to Leeds for work & shopping, and to a lesser extent, York, occurred over the decades. A Leeds (via Horsforth and Harrogate) local service was later bouyed by the construction of new housing along the line outside York, whilst the local Leeds service (via Wetherby) became popular with Leeds commuters there and terminated at Harrogate. Finally, a Leeds to Newcastle or Middlesbrough semi-express service ran via Horsforth, Harrogate and Ripon, connecting the stations to the North-East, and lately, destinations in South Yorkshire.

The amount of services passing through Harrogate - all stopping at the major station, placed a strain on a station with only 2 platforms, and trying to accommodate terminating local services from Wetherby. The aging station was largely demolished in the 1980s, and the station significantly redesigned. Gone were the 2 platforms, and 4 tracks in the station area (including 2 middle bypass tracks). The western bay platforms and redundant tracks disappeared, and land turned over to the council to create a larger bus station with more covered waiting areas. The platforms and trackwork were redesigned to give 3 platforms (the western platform being kept), with the eastern (Leeds-bound) track removed, moved to the east, and then an island platform inserted to give a central "terminating" platform. The station building was also demolished and rebuilt, incorporating new direct bridge links to the enlarged bus station, adjacent multi-storey car park, and a cross-road bridge to the town centre (and later also a shopping centre), giving a very small "Pedway" network.

Lincoln

An aerial view of Lincoln from decades gone by, showing both Central and St Marks stations.

Lincoln, for many decades, had the dubious honour of being endowed with two separate stations, catering to differing routes. Lincoln Central existed on the Northwest - Southeast axis (roughly Yorkshire to East Anglia), whilst Lincoln St Marks sat on a Southwest - Northeast axis (roughly East Midlands to the Lincolnshire coast). Although the lines intersected on a flat diamond crossing, causing a bottleneck, the stations remained separate until the 21st Century. Other branches from the two stations had, by then, closed; the branch network to Louth, Boston and Skegness was well gone, whilst the arrangement of Lincoln bypass lines around the town centre were on their last legs. The branch line to the west to Mansfield only existed in order to allow coal trains access to the significant power station complex at High Marnham. Upon closure of High Marnham during the 1990s switch from coal to gas, the site was procured by British Rail and used during initial experiments in to wind turbines and how much electricity they could contribute to British Rail (in order to reduce their energy costs). By now, the branch via Market Rasen to Grimsby was hardly used, with a very derelict station at Market Rasen; most rural passengers used Louth instead, which still retained direct London services from Grimsby, and there were few longer distance passengers from the Grimsby area to the East Midlands.

Whilst officially open, in the 1990s the Market Rasen branch was mothballed, it's role in the network dead with freight now running via Louth or Gainsborough (where a new short chord allowed multi-directional access), and very few passengers using Market Rasen station itself. The line to Mansfield also became redundant after the closure of High Marnham in the 1990s too, with the line to be closed - until the Mansfield Heritage Railway stepped in. The railway, using a site on the eastern outskirts of Mansfield on the former Mansfield Railway route, raised capital and acquired the line to Lincoln, as well as the rights to use the Lincoln St Marks site (as trains services east of St Marks towards Market Rasen were no longer operating). A new "Lincoln Rail 2010" plan was launched in 2000; works would be conducted to remove level crossings; both to the east (Great Northern Terrace - to receive a road overbridge), and in the town centre. The High Street crossing would be pedestrianised (in line with a local council objective) and replaced by a large overbridge, which would continue over Wigford Way / St Marys Street, although plans to close the Brayford Wharf crossing were voted down by the local council and the level crossing remains, albeit with a footbridge. The British Railways route from Newark now approached Lincoln in a slightly twisted fashion with a triangular junction, whilst the newly extended heritage line (now the Mansfield & Lincoln Railway) now using a bridge over the BR tracks, nicknamed the "ski jump" due to the gradients operated to Lincoln St Marks station. The M&L Railway has one of the longest stretches of double track of all British heritage routes, and operates intensively on summer weekends.

-------------

Well thank you for the honour in the Turtledove thread. In return, here's a bonus little chapter of material that I hadn't got round to fleshing out !

Harrogate is a semi-important junction stations, with a retained line via Wetherby and also via Ripon to the north. Lincoln is less busy; the line via Market Rasen has virtually closed - I'd bet there'd be "Mansfield & Lincoln Railway" people eying up an extension there, but at the moment it's just mothballed.

Thank you for the bonus chapter. The Turtledoe nomination is well deserved imho.

How did the experiments at High Marnham work out?

No grand Light Rail plans in the Lincoln area then.

Does Skeggy not have a rail line? I was sure it did...

Bet the 80’s rebuild station in Harrogate is boxy and ugly...

More please!

How did the experiments at High Marnham work out?

No grand Light Rail plans in the Lincoln area then.

Does Skeggy not have a rail line? I was sure it did...

Bet the 80’s rebuild station in Harrogate is boxy and ugly...

More please!

Share: